Accredited Debt Relief claims it can help you settle debts for 40-45% less than you owe but with settlement fees up to 25% and serious credit score impacts, is it worth it?

The Debt Settlement Reality

If you’re drowning in $10,000+ of credit card debt, debt settlement sounds tempting: negotiate with creditors to pay less than you owe. Accredited Debt Relief, founded in 2011, has helped over 700,000 customers manage more than $2 billion in debt. But debt settlement comes with major risks that could leave you worse off.

How Accredited Debt Relief Works

Here’s the process in simple terms:

1. You stop paying creditors. Instead, you deposit money into an FDIC-insured escrow account you control.

2. Your accounts become delinquent. This tanks your credit score sometimes by 100+ points.

3. Accredited negotiates settlements. As money builds in your account, they contact creditors to accept less than you owe.

4. You pay the settlement. If creditors agree (no guarantee), you pay from your escrow account.

Timeline: 24-48 months on average

Availability: 30 states plus Washington D.C. (not available in DE, HI, IA, MN, NH, ND, OR, RI, VT, WA, WI, WY)

What It Costs

Accredited Debt Relief doesn’t disclose exact fees upfront, but here’s what you’ll typically pay:

- Settlement fee: Usually 25% of enrolled debt (industry standard is 15-25%)

- Monthly account maintenance fee: Amount undisclosed

- One-time setup fee: Amount undisclosed

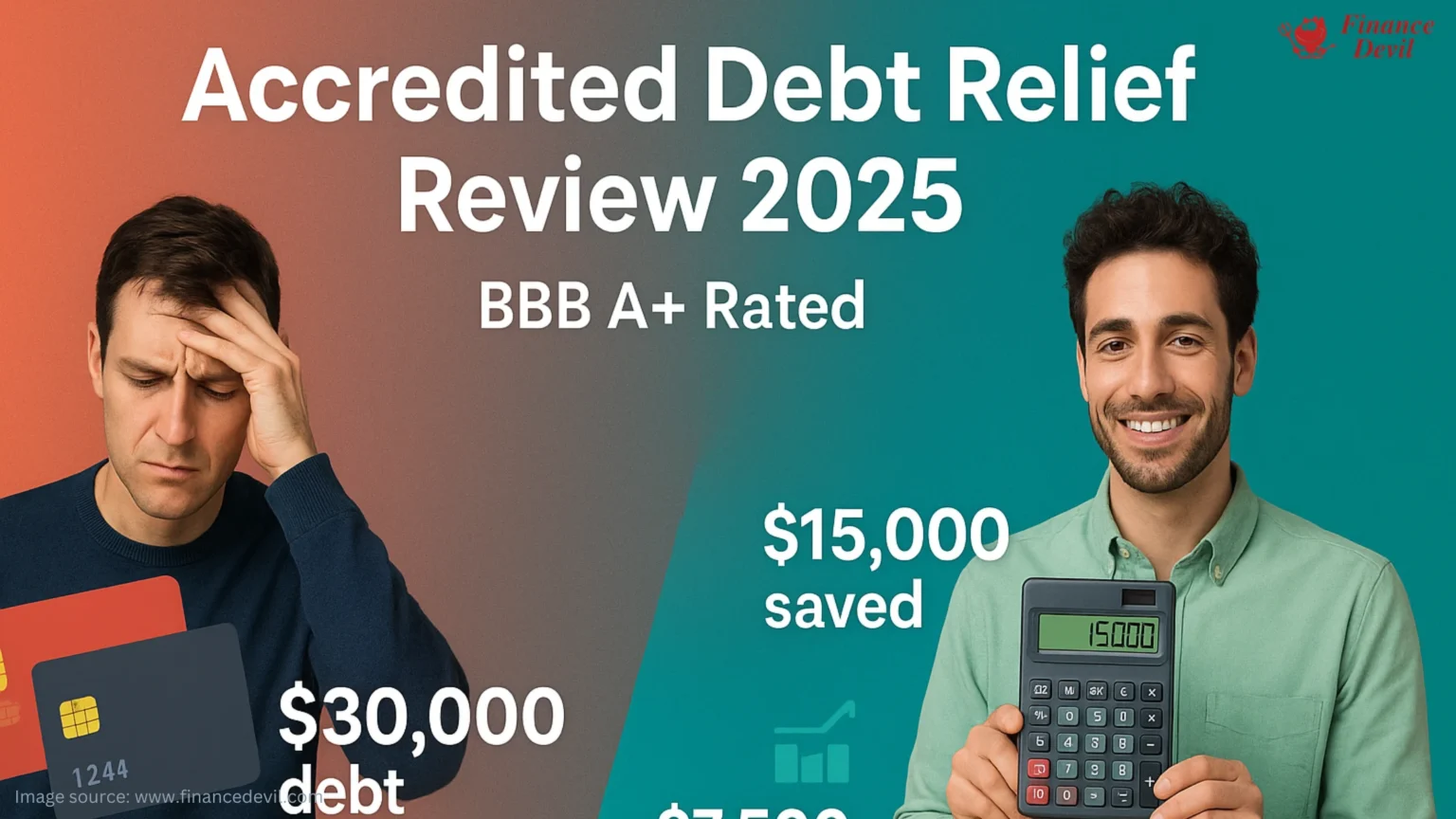

Example: If you enroll with $30,000 in debt and settle for $15,000, you’d pay:

- $15,000 to creditors

- $7,500 settlement fee (25% of $30,000 enrolled)

- Total: $22,500 (vs. paying the full $30,000)

Hidden costs: Late fees and interest continue piling up until settlement. Forgiven debt over $600 may count as taxable income.

Requirements to Qualify

- Minimum debt: $10,000 in unsecured debt

- Eligible debts: Credit cards, personal loans, medical bills, collection accounts, private student loans

- Ineligible debts: Mortgages, auto loans, federal student loans, secured debts

- Financial hardship: Must demonstrate you’re struggling to pay

Accredited does a soft credit check (no impact on your score) during application.

Accredited Debt Relief vs. Competitors

| Feature | Accredited Debt Relief | National Debt Relief | DIY Settlement |

| Minimum debt | $10,000 | $7,500 | Any amount |

| Avg. settlement | 40-45% reduction | 30-50% reduction | Varies |

| Timeline | 24-48 months | 24-48 months | Your pace |

| Settlement fee | ~25% (undisclosed) | 15-25% disclosed | $0 |

| BBB rating | A+ | A+ | N/A |

| States served | 30 + DC | 36 + DC | All |

The Major Risks

Credit damage: Expect your score to drop 75-150 points. Delinquencies stay on your report for 7 years.

No guarantees: Creditors aren’t required to settle. You might get sued instead.

Total costs: Between fees, interest, and penalties, you may pay more than your original debt.

Tax consequences: The IRS may treat forgiven debt as income (unless you’re insolvent).

Better Alternatives to Consider

Debt Management Plan: Nonprofit credit counseling agencies consolidate payments and reduce interest rates without settlement. Builds credit instead of destroying it.

Debt Consolidation Loan: Borrow at lower interest to pay off high-rate debt. Rates as low as 4.9% if you have decent credit.

DIY Debt Settlement: Call creditors yourself. Same results, zero settlement fees save thousands.

Bankruptcy: Chapter 7 erases unsecured debts in 4-6 months. Similar credit impact but faster resolution.

Customer Experience

Ratings:

- BBB: A+ rating with 4.89/5 stars (2,349 reviews)

- Trustpilot: 4.8/5 stars (7,492 reviews)

- ConsumerAffairs: 4.9/5 stars (2,449 reviews)

Pros praised: Empathetic customer service, knowledgeable representatives, daily support (8am-11pm EST weekdays)

Common complaints: Aggressive follow-up calls after initial consultation, lack of fee transparency on website

Frequently Asked Questions

Is Accredited Debt Relief legit?

Yes. It’s BBB-accredited with an A+ rating and accredited by the American Association for Debt Resolution since 2011.

What’s the minimum debt to enroll?

$10,000 in unsecured debt. National Debt Relief accepts $7,500 minimum if you need a lower threshold.

How much will my credit score drop?

Expect a 75-150 point drop initially. Negative marks remain for 7 years, though the impact lessens over time.

Can I settle debt myself?

Absolutely. You can negotiate directly with creditors and avoid the 25% settlement fee potentially saving $7,500 on $30,000 in debt.

Does Accredited Debt Relief work with all creditors?

No. Some creditors refuse to settle. There’s no guarantee of success, even if you complete the program.

What if I need to buy a home soon?

Don’t use debt settlement. The credit damage makes mortgage qualification nearly impossible for 2-3 years. Consider a debt consolidation loan instead.

Bottom Line

Accredited Debt Relief has strong customer reviews and legitimate credentials, but debt settlement should be your last resort, not your first option. The 25% fee, credit score devastation, and lack of guarantees make it riskier than alternatives like debt management plans or consolidation loans.

Best for: People with $30,000+ in unsecured debt and no assets to protect who’ve exhausted other options.

Not for: Anyone planning to buy a home, finance a car, or needing credit access within 3-5 years.

Ready to Explore Your Options?

Get a free debt relief consultation to compare debt settlement, consolidation loans, and management plans. See which option saves you the most money without destroying your credit.

Compare personalized debt relief quotes from top-rated providers and see your potential savings in minutes with no obligation.

In another related article, Pacific Debt Relief Review: Can You Really Cut Your Debt in Half?